There have been some significant moves coming from Alterra Mountain Company in the last 6 months and along with their Ikon Pass and they are poised to take over ski industry leadership status from Vail Resorts should they continue to execute their strategy effectively.

The news started last last September when Alterra announced that they would merge Deer Valley with the yet-to-be built Mayflower resort next door, creating North America's 4th largest resort with 5,726 acres of terrain and 37 lifts. A massive $3.2 billion of investments are planned, though Alterra is leaving the base village and real estate entirely to Extell Development Co., a New York City real estate developer who started the project in 2014. Likely less than 30% of the full cost of the expansion will come from Alterra and will be spread over 3 or more years. To put the size of this investment into context, Vail Resorts paid $1.1 billion for the 8,171 acre Whistler Blackcomb in 2016.

Near the end of January we got word that KSL Capital Partners, Alterra's majority shareholder, closed over $3 billion in a single-asset continuation vehicle for Alterra Mountain Company. This confused many who wrote about this and whom I spoke with, even a week later, and much of this confusion may have come from an early Ski Area Management Magazine article where there was significant speculation about what a potential cash infusion could be used for. In reality this was simply a way for some early investors to cash in their chips for a profit while new investors bought in. This 'vehicle' could have allowed them to raise additional capital for use by Alterra but there's no indication this happened, and there are other signs that it didn't which I will share below.

Then this Monday as the ink was still drying on on the continuation vehicle transaction we learned that Alterra will buy Ikon Pass partner Arapahoe Basin for an undisclosed amount which I would estimate to be somewhere between $125 million and $150 million based on multiples of their publicly disclosed $11.1 million EBITDA and the announcement of $110 million in profits from the sale by the current owner.

These are likely just the early stages of a new round of growth and consolidation in the ski industry that may result in Alterra surpassing Vail Resorts for market leadership within the next few years.

Who Is Alterra Mountain Company?

In April of 2017 KSL Capital Partners, a Denver-based private equity firm specializing in travel and leisure, and Aspen Skiing Company, a division of Henry Crown & Company and owners of Aspen Mountain, Aspen Highlands, Buttermilk, Snowmass, joined forces to buy struggling ski operator Intrawest, the then owners of Steamboat, Winter Park, Stratton, Snowshoe, Tremblant, Blue Mountain (Ontario), and CMH Heli-Skiing. The price was $1.5 billion plus the assumption of about $600 million in debt. At the same time it was announced that KSL's Squaw Valley/Alpine Meadows (now Palisades Tahoe) would also become part of the new entity. Just two days later they announced that Mammoth Resorts, owners of Mammoth Mountain, June Mountain, Snow Summit and Bear Mountain, was also being purchased by the new entity. In just a matter of 48 hours a new ski conglomerate comprised of 11 resorts and one heli-skiing operation had been created. The consolidation continued in August of that year with the purchase of Deer Valley.

Alterra Mountain Company was announced in January of 2018 as the name of the new venture and they also announced the Ikon Pass as a successor to the M.A.X Pass starting the following season. Later that same year they continued their buying spree by purchasing Crystal Mountain and Solitude, and in 2019 came Sugarbush. Acquisitions were paused after the pandemic started, but in 2023 they resumed with Schweitzer and now Arapahoe Basin bringing the total to 18 ski operations.

Rusty Gregory, who worked his way up from a liftie at Mammoth Mountain to its CEO, became Alterra's first CEO in 2018. Gregory retired in 2022 and was succeeded by Alterra's President, Jared Smith. Smith came from Ticketmaster where he worked for 17 years and last served as their president and chairman.

KSL Capital Partners is the majority owner in this venture. They are a private equity firm which seeks investments from public and private sources to fund ventures, grow their value, and return profits to the investors. The company's roots go back to 1992 when Wall Street investment firm Kohlberg Kravis Roberts & Co. entered a partnership with Vail and Beaver Creek executives Michael Shannon and Larry Lichliter to establish KSL Recreation Corporation. "KSL" stands for Kravis, Shannon, and Lichliter. Their company was eventually sold in 2004 to to CNL Hospitality for $1.4 billion, and subsequently the new entity of KSL Resorts was founded by Michael Shannon, Eric Resnick, and Scott Dalecio who is its current president and CEO.

KSL Capital Partners, not to be confused with KSL Resorts, was founded in 2005 by Michael Shannon and and Eric Resnick. Shannon serves as their chairman, and Resnick serves as their CEO. Today KSL Capital Partners manages $21 billion in assets and has invested in over 165 different businesses with Alterra Mountain Company being the largest by far. KSL Resorts, an affiliated entity who specializes in hotel and resort management, purchased Camelback in 2019 and Blue Mountain (Pennsylvania) in 2021, and starting this season both resorts were added as limited partners on the Ikon Pass offering either 5 or 7 days of access to each.

KSL Capital Partners' founders came from the ski industry. Michael Shannon was CEO of Vail Associates, owners of Vail Mountain and Beaver Creek, from 1986-1992. Eric Resnick was VP of Strategic Planning for Vail Resorts in their early days from 1996-2001.

Alterra's destiny is surely to become a publicly traded company. That's how KSL Capital Partners' investors in Alterra will realize gains on their investments. A few years ago at an annual company meeting Alterra's leadership indicated that they would not be going public for at least 5 more years and the recent continuation vehicle is a sign that it will likely be at least several more. If they put their cash to good use and maintain a strong growth trajectory, they could well see a valuation in excess of that of Vail Resorts when that happens and it is possible their implied value is already close to Vail Resorts' $8.4 billion market capitalization.

So far in their short 6 year history Alterra's execution from the bird's eye view has been nearly flawless and the stock market loves both growth combined with premium offerings, but they want to continue to build even more value before the current investors cash out and that would come by completing projects like the Deer Valley expansion and continued acquisitions. Popular opinion seems to be that a public offering will happen near the end of this decade.

Alterra and Vail Resorts By the Numbers

Since Alterra is a non-public entity there is far less information available regarding their finances, revenues, earnings, pass sales, etc., however they are large enough that they must rely on the bond markets to raise money which requires them to make disclosures so that ratings agencies can estimate their creditworthiness.

Jason Blevins of the Colorado Sun dug through the prior periodic review from Moody's when it was announced that Alterra would take over the Mayflower Resort's ski operations last summer and provided contrast with Vail Resorts in order to put this into perspective.

Moody’s Investors Service, which rates debt for bond investors, in May reported that Alterra generated $1.7 billion in revenue between January 2022 and January 2023. Moody’s reported Alterra had $1.1 billion in cash in January 2023 and the new loans would bump that to $1.3 billion with access to the $500 million loan due in 2028.

For comparison, Vail Resorts, the largest resort operator in North America with 37 ski areas, reported $2.5 billion in net revenue for its fiscal year 2022. In April, Vail Resorts reported $896 million in cash and access to about $630 million in debt.

At that time Alterra owned 16 ski operations vs. Vail Resort's 40 but managed to reach almost 70% of their revenue. The difference is that Alterra owns primarily destination resorts while about half of the ski areas in Vail Resorts' portfolio are quite small, located in the Midwest and Northeast, receive less than 250,000 skier visits per season and in many cases significantly less, and contribute far less per skier visit to their bottom line than destination market skiers and riders. These ski areas do help sell Epic Passes and boost other metrics while increasing perceived value for that product, however many of these 'eastern feeders' lack the same degree of ancillary revenue opportunities as destinations and attract skiers from their surrounding area who do not spend as much as those who travel long distances to take vacations. It's a different approach to the industry and driven by volume, discounting, and control of regional markets connected to urban centers, and it has proven to be a difficult strategy for them to manage. While both strategies on paper have significant potential, thus far the more destination-focused approach of Alterra that values quality over quantity and is priced at a premium to their competition seems to be more successful in practice, though in all fairness that's speculative due to a lack of visibility into Alterra's full financial results.

Moody's provided an update on Alterra's credit rating just this last Monday when the company secured an additional $200 million on one of their loans, likely associated with the purchase of Arapahoe Basin. Let me pause here for a moment. If the continuation vehicle provided additional working capital, it wouldn't make a lot of sense for them to increase their borrowing just a week later. KSL Capital Partners' own press release clearly stated that the continuation vehicle was offered in order to "return capital to limited partners". So it's fair to assume the continuation vehicle provided no additional working capital to Alterra.

In the credit rating update Moody's indicated that Alterra's debt-to-EBITDA ratio had increased to over 6x which Moody's indicated was primarily due to a short-term change in management compensation associated with exits, and they also described Alterra's financial policy as "aggressive under its private equity ownership with frequent debt add-ons to fund acquisitions, capital spending, and sizable cash outflows for management incentive plans over the next few years." Alterra in fact maintains over twice the debt-to-EBITDA of Vail Resorts, but the company is on a rapid growth trajectory, investing sizeably into their operations, and they likely still have more cash on hand at this time than Vail Resorts, though Vail Resorts could likely raise significant amounts of capital without issue if they so desired.

While being over-leveraged has been the downfall of the likes of American Skiing Company, Intrawest, and even Peak Resorts, when paired with Alterra's well executed acquisition and growth strategy during a time of record interest in the sport the level of leverage seems to be well-suited for the current environment and there are many similar companies with twice that leverage. Alterra's owners can offset their debt by selling interest in the company should they so choose, but selling stakes in the company dilutes the equity of the current shareholders. The fact that they did not seek to raise more capital at this time suggests that Alterra has access to enough capital or can at least borrow what it needs to fund their growth strategy. Alterra has an advantage over Vail Resorts in that they don't need to impress investors once every 3 months with their financial results, they don't use their earnings to pay out dividends to shareholders, and they aren't buying their own stock in order to increase shareholder equity. We're talking many hundreds of millions of dollars per year that can be reinvested. Alterra's present ownership structure is a distinct advantage in the current environment.

Alterra's investments in capital projects this year will total a whopping $490 million, and their investments in Steamboat alone during the last 3 years total more than Vail Resorts budgeted across their entire portfolio this year; just $211 million. That's a level so low that not only do they risk falling behind their big-spending competition in terms of modern amenities, they may be deferring lift replacement cycles and borrowing from their physical assets in order to boost earnings and return proceeds to shareholders. Last year Vail Resorts spent about $814 million on dividends and buying back their own stock, constituting almost all of their earnings while reducing their cash and providing zero benefit to growth in an increasingly competitive landscape. This pattern of significant outflows to shareholders and tepid investments in capital projects has gone on for many years and makes them vulnerable as the industry's leader.

What Are Alterra's Plans for the Future?

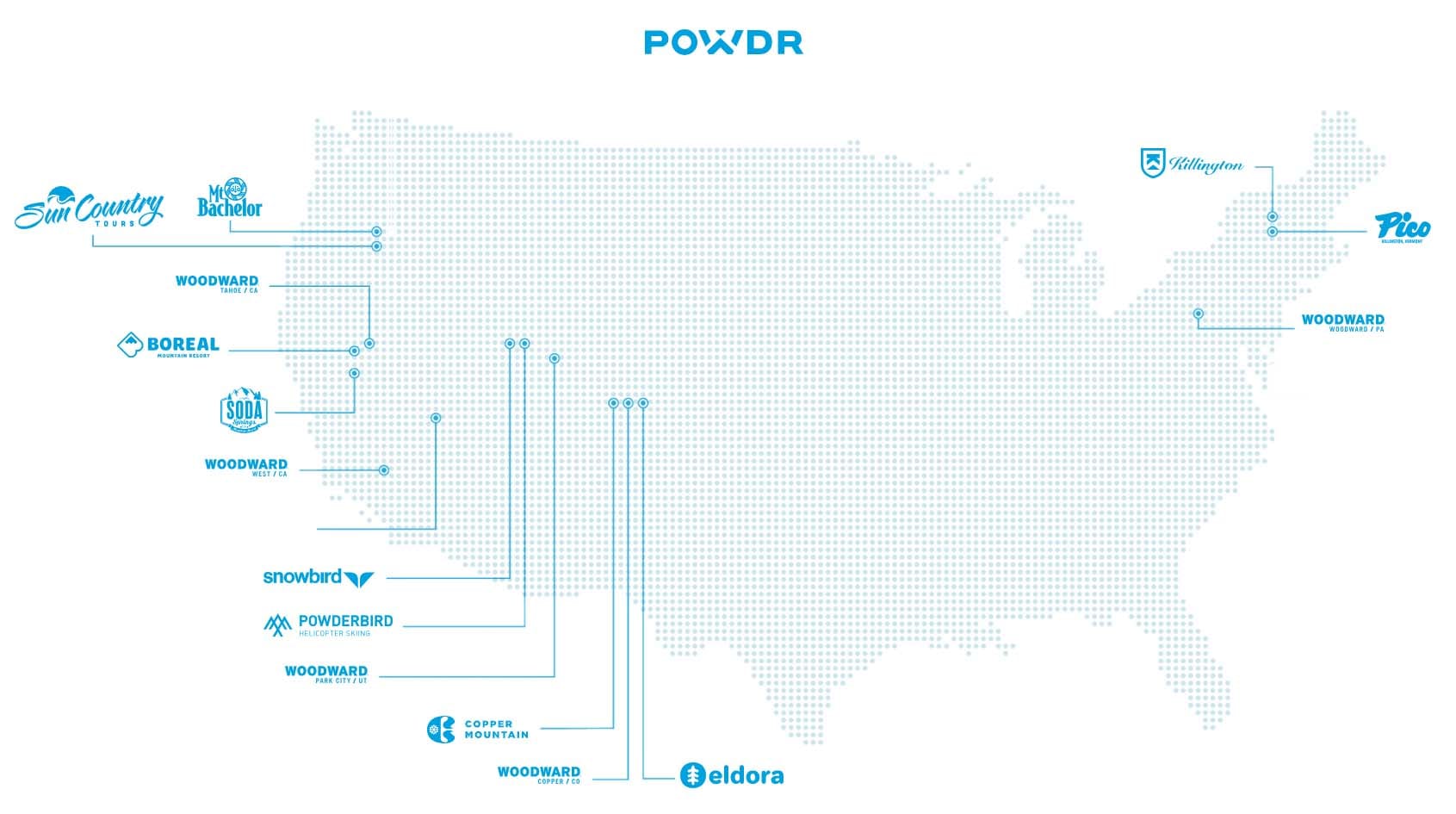

Alterra partners with other conglomerates like Boyne, POWDR, Aspen Skiing Company, large independents, and international destinations in order to build their Ikon Pass portfolio, making their pass attractive and very competitive with the Epic Pass for destination skiers and riders without overextending themselves. This strategy however comes at a cost of double-dipping into the pass revenues. Non-owned resorts likely see somewhere between 30%-40% of their rack rate as compensation from Ikon Pass usage. This isn't as paltry as it may sound due to day ticket price inflation and the introduction of variable pricing strategies which leaves yields much lower than the rack rate. Since Alterra's Ikon Pass with its over 40 non-owned partner resorts is primarily paying out to third-parties under this model, owning more of the resorts on the pass would cut out revenue lost to partners and grow their own profits faster.

If you ask around the industry for opinions on what Alterra's next move may be, buying POWDR is at the top of almost everyone's list. Ski Area Management Magazine shared the following in a recent article on Alterra's continuation vehicle funding.

"The most-mentioned targets include the usual multi-area suspects, from POWDR to Sun Valley/Snowbasin. As one source said, "there are not many big targets out there."

Sun Valley and Snowbasin wouldn't really move the needle much so they don't seem like top targets to me, but POWDR looks like a home run as the top acquisition target since 6 of their resorts are on the Ikon Pass and both Eldora and Copper Mountain are unlimited despite not being owned by Alterra. Owning those properties along with Arapahoe Basin, Steamboat, and Winter Park in Colorado would not change the pass landscape for consumers, but it makes POWDR even more valuable to Alterra than just the assets themselves because they could keep significant additional revenue. In the Northeast having POWDR's Killington and Pico as unlimited partners on the Ikon Pass would probably make their pass more attractive than Epic Pass for big mountain skiing in the Northeast, and moves like that can dramatically reshape the pass landscape where presently there are only two unlimited options on Ikon.

POWDR hasn't been partaking in the consolidation in the industry outside of joining the Ikon Pass and has focused most of their expansion efforts on Woodward facilities instead. They seem ripe as an acquisition target and they are worth more to Alterra than anyone else. POWDR sees about $300-350 million in annual revenue based on extrapolating from a 2021 baseline of $256 million reported by Moody's. They probably see somewhere above 3 million skier visits across their resort properties with a sizeable percentage coming by way of the Ikon Pass. No other ski resort operator is more tied to the Ikon Pass than POWDR.

How much might POWDR sell for? Well, valuations in the last decade for larger resorts have skyrocketed as a result deep-pocketed industry consolidation led by none other than Vail Resorts and Alterra. Based on more recent examples I'm would guess that the present going rate would be around $1.5 billion given that POWDR's 3 largest resorts each see around double the visitation of Arapahoe Basin and likely have stronger ancillary revenue opportunities. This is inclusive of full ownership of Snowbird which is majority owned by POWDR's founder, along with adjustments for debt.

In the Northeast another possible acquisition target may be the KSL Resorts properties of Camelback and Blue Mountain in Pennsylvania. These are not part of Alterra despite their owners having an affiliation with KSL Capital Partners and having been added as limited Ikon Pass partners starting this season. On the surface adding these two popular resorts to the Ikon Pass makes the pass more attractive in the region and helps funnel more people to higher profit western destinations, but they need to be very careful about being identified as the cause of widespread grief among existing patrons. Vail Resorts has already taught us that excessive crowding is not well tolerated in the Northeast. What happens in Salt Lake City, Denver, Seattle, and Tahoe is not the norm east of the Rockies and many in the Northeast have alternatives close enough to consider.

I'll be honest here, I actually view the inclusion of these resorts on the Ikon Pass to be a mistake for both Alterra and KSL Resorts as implemented. These resorts were already very busy to start and the excessively bursty traffic at these two resorts this season has led to several sold out days at Blue Mountain along with many complaints online about lift lines, dangerous overcrowding on the slopes, and even reports of difficulty in leaving the resort. Neither resort seems to have needed to add excess discounted traffic on weekends, but if this was helping to sell more Ikon Passes and they were owned by Alterra, the discounting could be a net gain.

Their inclusion on the Ikon Pass however is another sign of Alterra softening their stance on including non-destination resorts in recent years. It's hard to say confidently if they would or wouldn't have included these two resorts had they been owned by a different entity, but if this is in fact a change in strategy by Alterra to include more regional destinations as a way to boost pass sales, Alterra buying these two resorts might make sense, and there is an easy fix for excessive demand that former Alterra CEO Rusty Gregory shared in the most basic of terms in a roundtable discussion with Jason Blevins back in 2022.

"When things get too busy the price needs to go up."

-- Rusty Gregory

Excessive demand is not a problem; it's an opportunity to make more money. I wish everyone in the ski industry would realize that. Capacity can be controlled, the pandemic taught us that, and it's being practiced at multiple Alterra-owned resorts, Ikon Pass partners, Indy Pass partners, and others. Skiers and riders seem to respond positively to controls if they limit the pain of overcrowding. If Alterra and KSL Resorts continues to approach the Northeast in this way; well, I've got another Rusty Gregory quote from that same roundtable discussion that applies in a broader sense.

"You can see resorts that play the aggressive card too often and push too many people around. During times like this, they're getting their politics handed to them in a very difficult way and are paying the price."

-- Rusty Gregory

They probably have until next season starts to figure out a way forward that doesn't damage the reputation of KSL Resorts, Ikon Pass, Camelback, and Blue Mountain. They'll probably be forgiven if they do, and the implementation can be as simple as limiting Ikon Pass redemptions, limiting day ticket sales, utilizing parking reservations, and/or raising pass and ticket prices.

I've also heard rumors from an industry insider of another a medium-sized Northeast resort being an acquisition target for either Alterra or KSL Resorts (I suspect the latter given the likely target). Discussing who this might be would be speculative as the target wasn't identified by name. If that does happen, it will likely happen before the start of the following season.

Alterra could become the dominant force in the Northeast in a very short period of time should they snap up POWDR, Camelback, Blue Mountain, and possibly others, making them unlimited on one version of the pass or another. That would cause a fundamental shift in the Northeast pass market and create more opportunities for Ikon Pass to bring skiers and riders out West where they spend more money. The entry of KSL Resorts into the fold creates opportunities for synergies between the two, possibly allowing Alterra to grow without being bogged down by managing a larger portfolio. They likely have the capital or credit to acquire the non-POWDR properties as is, and there are multiple ways they could finance a POWDR acquisition ranging from an exchange of equity, equity funding, or bonds.

This may just be me and others overthinking the situation. The confusion over the $3 billion continuation vehicle certainly got people speculating about where they might spend a large sum of money, myself included, but if aspirations exist to both consolidate more western properties while becoming a dominant player in the Northeast market, this seems like a plausible way to get that done. Alterra just bought themselves at least another 5 years to appreciate in value and they sure aren't going to sit on their hands, nor are they going to appreciate much in value by buying a small number of non-leading destinations who do little to make the Ikon Pass more popular. They are going to continue to make bold moves that will reshape the ski industry for years to come.

Final Thoughts

It's not necessarily my desire to see this level of consolidation in the Northeast market, but a duopoly is far better than a monopoly because consumers generally benefit from competition, and I do believe Vail Resorts has proven that eastern feeders as a part of a mega-multi-pass is a strategy that has legs despite the negatives that many have experienced as a result of how that strategy has been implemented.

I am not a fan of the volume over quality approach to the ski industry. Ski areas are not amusement parks (except maybe Camelback, no shade intended), and the East is fundamentally different from the West. We are primarily day-trippers and weekenders, and we generally have an affinity to the ski areas themselves and not the brand that owns them nor the pass they are on. Alterra understands how to maintain the character and uniqueness of their resorts with the proper balance of oversight and local decision-making. Growing their footprint while showing success beyond their balance sheet would hopefully teach others the right path to success. Alterra has clearly shown themselves to be successful without trying to recreate the ski industry as Disneyland or Six Flags, and they don't see themselves as a subscription service. They know the ski industry, they know their customers beyond their Net Promoter scores, they have been responsive to overcrowding, and they see excess demand as an opportunity to increase profits and expand terrain instead of just uphill capacity. Skiing is not a commodity, it's a limited resource that in many cases is in high demand and holds significant opportunity.

Now don't get me wrong, I'm far from a corporate shill, but I'm also a realist and appreciate the positive parts of capitalism. I don't love the big corporate side of the ski business; it scares me in fact and I don't feel safe on some slopes now as a result of greed, but we live in a capitalistic society and so far I'm OK with Alterra's measured approach to growth and competition in the East. I like the fact that our fruit doesn't hang very low causing us to be overlooked by western-based conglomerates when it comes to massive projects that can be disruptive to communities, and I love the fact that we have so many choices and so much variety. I have learned to appreciate them all. If I lived in the West I would need to come to terms with how populations and interest in skiing are growing at a rate far in excess of supply, and I would probably have some appreciation for Alterra showing a degree consciousness of their effect on the communities in which they operate and are looking to provide a skiing experience that I might enjoy. The "don't come here it sucks" and "multi-passes ruined everything" crowds are impossible to satisfy because they don't appreciate the codependency with the business side of the equation, but in some cases they are of course right. Multi-passes are not fundamentally bad; they have made skiing more affordable and are boosting an industry that was shrinking and growing older. They're only bad when when care is not used to attempt to balance everyone's needs.

I must confess that I would not be doing what I am doing today if not for the M.A.X Pass allowing me to affordably visit so many places that I otherwise would not have. Balancing the needs of skiers, communities, and business is the key to success in this industry, and I hope Alterra continues to appreciate our shared interests and play the long game because they are now poised to become the new industry leader if they do.

-- Matt

Comments ()